The Ministry of Finance Malaysia has published the 2023 Pre-Budget Statement to share the direction and focus for the 2023 Budget. The themes for 2023 are Strengthening Recovery, Facilitating Reforms Towards Sustainable Socio-Economic Resilience of Keluarga Malaysia.

This document also provides updates on key initiatives implemented under Budget 2022 and the stimulus and assistance packages.

Deloitte Malaysia Tax Services has released its latest Tax Espresso – Special Alert bulletin update. This release covers Global Minimum Tax (GMT) and BEPS 2.0 along with Deloitte Malaysia’s tax experts recommendations.

What is Global Minimum Tax (GMT) and who will be affected?

GMT under Pillar Two is a once-in-a-lifetime global tax reform, meant to end tax competition and profit shifting. It is aimed at ensuring that multinational companies (MNCs) pay the right amount of taxes, that is at 15%, regardless of where they operate. While an MNC group can operate in low-tax, high-tax, zero-tax country or in a country that offers tax incentives, the universal GMT rules would kick in to ensure 15% tax is paid.

GMT applies to MNCs operating in at least two jurisdictions, with an annual consolidated group revenue of at least €750 million (approximately US$ 804 million) in at least two of the four immediately preceding fiscal years. Two categories of MNCs that need to be fully aware of the impact of GMT – large Malaysian-based MNCs that have foreign operations and foreign-based MNCs that have operations in Malaysia.

Will Malaysia implement GMT?

While Malaysia is not a member of the Organisation for Economic Co-operation and Development (OECD), it is a member of the OECD’s Inclusive Framework. There is thus an expectation that it will support and implement the GMT. From the very outset, we were clear that there is also no reason for Malaysia to avoid GMT implementation as the taxes that could have been collected here will be ceded to other jurisdictions.

On 3 June 2022, the Ministry of Finance (MOF) Malaysia released a pre-budget statement which shared that Malaysia is currently reviewing the technical details of the GMT. Malaysia acknowledges the OECD’s original plan of implementing GMT in 2023. The OECD has a very ambitious timeline in GMT implementation. The Income Inclusion Rule (IIR), being the main rule, is to be rolled out in 2023, while the backstop rule – the Undertaxed Payments Rule (UTPR) – is targeted to be implemented the following year. All rules operate as “top-up” to a minimum tax of 15%. Malaysia will need to amend its domestic tax legislation to implement this. A point to note is that there is a plan for the European Union to defer this by one year and it remains to be seen as to how this will affect Malaysia’s roadmap on GMT.

Similar to Hong Kong and Singapore, the possibility of Malaysia introducing Qualified Domestic Minimum Top-up Tax (QDMTT), being part and parcel of the GMT, was also mentioned. This is not unexpected as QDMTT serves as a mechanism which will enable Malaysia to absorb the potential top-up taxes payable that may otherwise be ceded to other countries.

In our view, the MOF’s statement is useful and timely as it sheds light on Malaysia’s direction on GMT. It provides some level of certainty for the large Malaysian-based MNCs and foreign-based MNCs that operate in our country.

Pillar One

Concurrently, Malaysia is also reviewing the technical details of Pillar One which introduces a new mechanism for allocating profit, which applies to MNEs with global revenue above €20 billion (approximately US$ 21 billion), and profit before tax above 10%, with 25% of profit above the 10% threshold (i.e., Amount A) to be reallocated to market jurisdictions. Pillar One also contemplates simplifying the application of the arm’s length principle to in-country baseline marketing and distribution activities (Amount B), with further details to be developed. Pillar One also outlines a proposed approach to mandatory binding dispute prevention and resolution for Amount A.

What is next for large businesses?

With the pre-budget statement, the key question as to whether Malaysia will ever implement GMT, including QDMTT, has now been answered to a certain degree. The two categories of MNCs mentioned earlier should start to prepare for this. Early understanding of the impacts of GMT and preparation will be key to an effective and efficient implementation.

These are our recommendations:

- Perform impact assessment on a group-wide perspective and identify risk areas.

- Identify entities within the group that would be obliged to pay the top-up tax (whether to the Malaysian or foreign tax authorities) and determine the impact on cash-flows and functions.

- Assess the impact on dividend distribution to shareholders.

- Quantify potential impact by undergoing a modelling exercise.

- Understand how local authorities in the different jurisdictions where the group operates may respond (e.g., whether they will introduce their own domestic minimum tax or revamp their tax incentive regimes) and analyse the different scenarios.

- Analyse if there is a need to renegotiate tax incentives granted or to replace them with non-tax incentives such as grants. A company in a country that enjoys tax incentive is likely to have an effective tax rate (ETR) that is below 15%. However, this does not mean that there will be a top-up tax as one needs to compute ETR on a jurisdictional basis, meaning ETRs of other companies in the same country will also need to be factored in. The significance of economic substance needs to be understood as it is useful to minimise the top-up tax.

- Analyse if the present accounting system of the Group would be able to generate the data required for the purposes of GMT.

- Be prepared to lodge GMT filing, as this is required regardless of whether there is a top-up tax or not. While the first GMT filing is only due 18 months after the financial year end, there is a critical need to understand the full impact of GMT.

The way forward

There is no reason for Malaysia not to adopt GMT. It is just a matter of timing and certainly, the MOF’s pre-budget statement has shed some light on Malaysia’s direction. GMT is just around the corner. Upon understanding the impact of GMT, time will be needed to configure the accounting system so that it can generate the data required for GMT, followed by trial run. All in all, the time is now for affected MNCs to act. A wait and see approach may no longer be tenable.

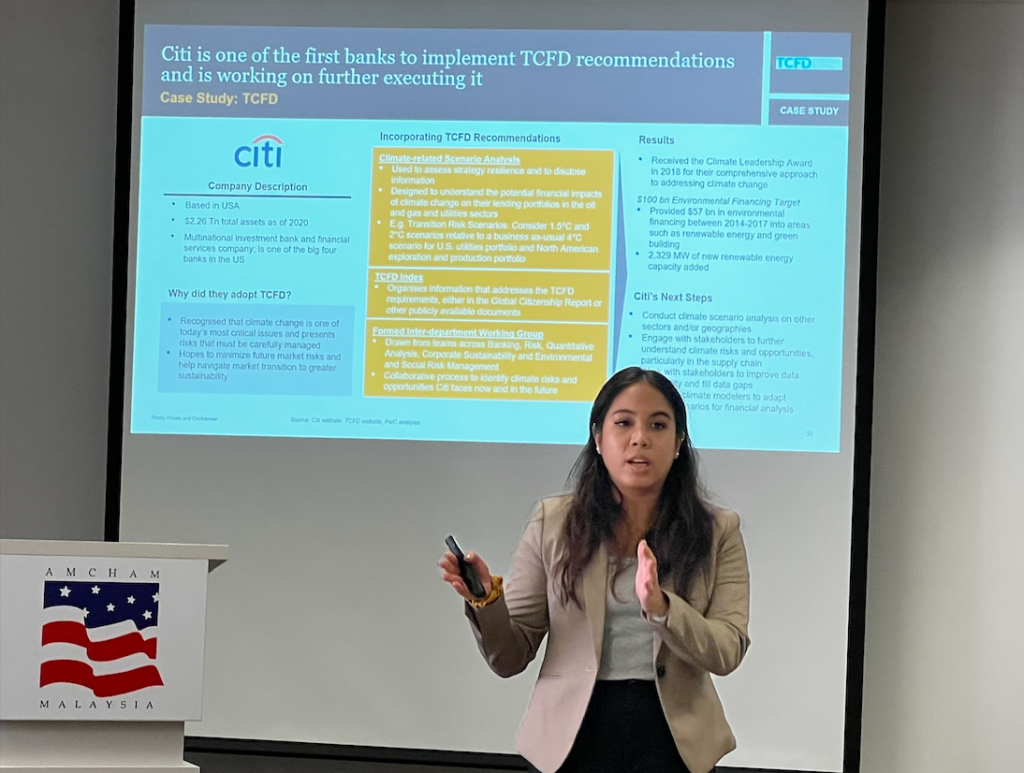

AMCHAM held its first Environmental Sustainability Governance (ESG) workshop today, titled ‘Deciphering the Alphabet Soup of Sustainability Frameworks’, as part of our ongoing ESG Program for 2022.

Rakesh Mani, Director, PwC South East Asia Consulting kicked off the session with the latest trends in sustainability and ESG along with what shareholders and consumers alike look for with brands. Vanessa Raju, Manager, Sustainability and Climate Change at PwC Malaysia and her team presented attendees with applicable frameworks and examples of companies that have implemented them.

Special thanks to all our presenters for making our first ESG workshop a success. Be on the lookout for the next ESG workshop.

Recently, a dozen OIS students and staff spent the day with local organizations learning about different ways to combat hunger. In the morning, students spent time serving at Kembara Kitchen’s community farm. Afterwards, students learned how Kembara Kitchen uses community partners and creative solutions to solve food shortages during times of crises. After weeding in the garden, students and staff brought over RM700 of food donations to Kembara Kitchen’s warehouse while learning about the logistical considerations involved in combating the Zero Hunger SDG.

At lunch time, the OIS team headed back to school, but their day was not done. For lunch, Oasis invited the Picha Project to campus to teach students how to make shawarma and how the organization is empowering refugee women in KL through a creative marriage between social entrepreneurship and food. It was an amazing day of serving, learning, and food.

Rajah & Tann Asia’s member firm, Christopher & Lee Ong, recently contributed an article titled “MICECA – Key to expanding India-Malaysia economic and trade ties” to the India Business Law Journal, a leading legal magazine in the region.

In this article, Partners John Rolan and Lim Siaw Wan, alongside pupil Loh Yan Shuang, explore how MICECA continues to play a significant part in fostering India-Malaysia bilateral relations and in expanding the economic and trade ties of these two nations.

Prime Minister Datuk Seri Ismail Sabri Yaakob on Tuesday (May 31) held talks with representatives of U.S. memory chip maker Micron Technology Inc to explore the potential for the company to increase its investment in Malaysia.

The delegation from Micron led by the company’s executive vice president of global operations Manish Bhatia met the Prime Minister in Putrajaya, following the latter’s recent working visit to the U.S.